Inflation isn't transitory anymore

Inflation isn't transitory anymore

Interest rates need to rise, and fast

Canadian inflation was 5.7% in February, the highest in over 30 years. When inflation jumped from its pandemic lows in the spring of 2021, the Federal Reserve (in)famously described it as transitory. At the time, inflation in the U.S. and Canada was being driven by huge price increases in a few pandemic-impacted categories along with ‘base effects’ as prices normalized from 2020. The message from central banks was that these kinds of localized, short-term price gyrations were to be expected as we came out of the pandemic, and that it was appropriate to “look through such temporary movements in inflation”.

That story is now over and price increases are everywhere. The Consumer Price Index (CPI) is a basket of goods and services and we use changes in its price to measure inflation. In February 2022, four-fifths of the basket had year-over-year price increases greater than the 2% Bank of Canada inflation target, two-thirds of the basket was rising by more than 3%, and a quarter of it was rising by more than 10%! When inflation hit the radar in early 2021, price increases were highest in historically high-volatility segments like gasoline and fresh food which tend to provide a poor signal of underlying inflation. Economists strip out these volatile components to compute ‘core’ inflation and get a better sense of underlying price movements. In February it was running at 3.9%.

While some prices move around quickly, there are others which tend to move very slowly. Trends in these components especially are a bellwether for something more fundamental happening the economy. The largest of these components are housing related (including rent and homeowner’s replacement costs), but also include personal health care, restaurants, and some household products. After decades of plodding along at about 2%, these low-volatility prices are spiking too.

Supply Chains

In 2021, the story was all about supply chains. Prices were rising because lockdowns had shuttered factories causing shortages of critical components, especially semi-conductors. No semi-conductors means no new cars and hence a spike in used car prices. Shortages were compounded by capacity issues at ports and in the trucking industry. To get a handle on these impacts, the Federal Reserve started computing a measure of supply chain disruptions based on the cost to ship raw materials, container shipping charges, and delivery times and order backlogs from producers.

You can tell at a glance that the pandemic badly frayed global supply chains. However, if you look closer, puzzles emerge. Supply chains were disrupted as early as January 2020, but inflation didn’t begin until the spring of 2021. Disruptions in Europe have eased (this data ends in February and doesn’t yet include the war in Ukraine), but the last inflation readings in the United Kingdom and Euro Area were 5.4% and 5.8% respectively. Moreover, when supply for a given product is reduced, you’d expect a one-time price increase as supply and demand reach a new equilibrium. We wouldn’t expect prices to rise continuously.

Something else is going on here.

A Wave of Demand

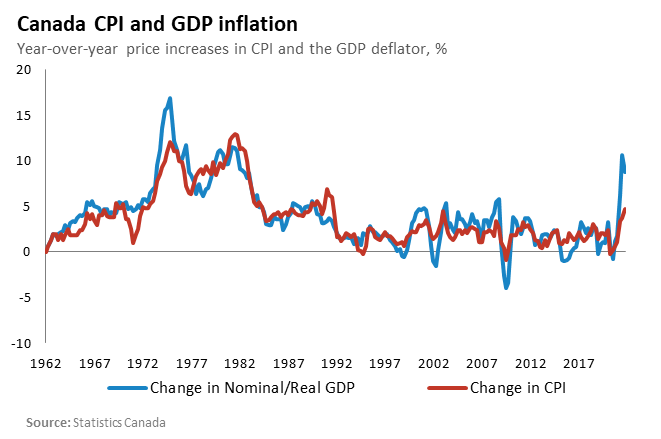

In the broadest sense, total economic supply — all the goods and services produced in the economy — is GDP1. People, firms, and governments buy the goods and services produced with money, the sum total of which is nominal spending. The gap between the growth in nominal spending (nominal GDP) and real production (real GDP) is the increase in the price level2. This isn’t the same thing as CPI measured inflation because it includes prices paid by producers too3 but over the long run its pretty close.

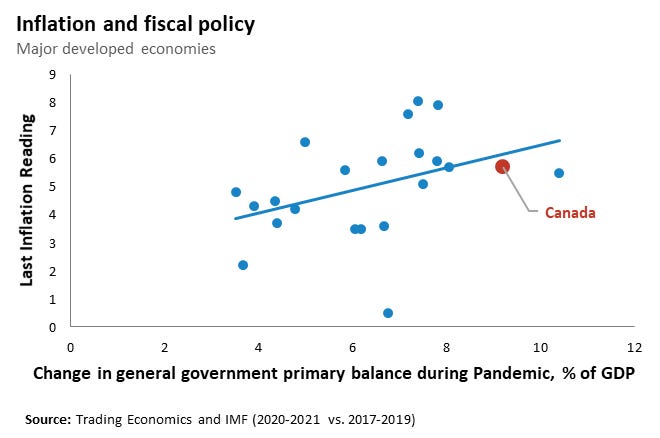

The price level in the economy is determined by the ratio of nominal spending to real output. The supply chain argument is that real output has been impaired, causing prices to rise. While there is a lot of truth to this, and our economic potential probably has been damaged by the pandemic, real GDP has now more than surpassed its pre-pandemic level. The more important cause of rising inflation at this point is strong demand. The unemployment rate is low, and industry and construction are operating near top speed4 and still the economy can’t produce enough goods and services. This is the reason why prices are rising: nominal spending is 11% higher than in 2019. Across the developed world, nominal incomes fell somewhat during the pandemic, but governments stepped in with vast fiscal stimulus. That money flowed first into savings and now it is driving consumption. Country by country, the larger the fiscal support, the higher inflation is now.

In Canada the wave is coming from consumers supported by past government spending. In 2019 Canadians earned about $1.5 trillion, paid $200 billion in net taxes5, and spent all of what was left — i.e. not counting additions to pension plans, the savings rate was about 0%. In 2020, earnings fell slightly but net taxes plunged thanks to CERB and other programs, so household disposable incomes jumped. They continued to rise in 2021 as people got back to work. At the same time, consumption was suppressed, so Canadians saved almost $300 billion. Now that the economy is reopening, households are unleashing a torrent of spending supported by both higher incomes and their savings.

Before we get to what central banks are thinking and what they should do next, a brief digression on the causes of inflation.

What causes persistent inflation?

Put simply, there are two longstanding schools of thought as to where inflation comes from. The first is Monetarism as propounded by Irving Fisher and Milton Friedman. Under this theory, the money supply determines the long-run price level (along with short-term dynamics). Increase the supply of money and ultimately you increase inflation6, hence Friedman’s quote “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

This isn’t the whole story though. After all, if you printed a trillion dollars and then stashed it in your account at the Fed mattress, there would be no mechanism whereby it would raise prices. You need a second element which I’ll call Demand Pull and is usually associated with Keynesian economics. In this theory changes in aggregate demand are the source of changes in inflation. Because one person’s spending is another person’s income, higher spending (demand) by households, governments, or firms will lead to higher nominal incomes. This spending can be facilitated by credit creation by banks via the money multiplier. If the economy is operating below its capacity, demand causes firms to hire workers and increase real production. Once the economy’s capacity is reached however, incremental demand still raises incomes, but it does not lead to further increases in production (at least in the short-term) because supply is constrained, instead it bids up prices causing inflation.

To these old theories, new elements have been layered in over time. The most important of which is the role of expectations which were recognized following the Great Inflation of the 1970s. At that time, governments and central banks assumed there was a direct tradeoff between inflation and unemployment. Increasing the rate at which money is created and spent causes higher inflation, but the added demand also creates jobs. Given the choice, policymakers chose low unemployment. By the late 1970s however, it had become clear that it was only unexpected changes in inflation which mattered. Workers and firms would notice inflation was high and bargain for wages and prices to match, through large cost of living adjustments for example. When the 1973 oil shock caused a slowdown in the economy, inflation was running at over 8% and unemployment was rising: Stagflation had arrived. Once people came to expect high inflation, lowering those expectations was a matter of a painfully high interest rates. To understand why, consider a typical worker in the mid-1970s was probably getting a 6-8% raise each year. If they didn’t get it, that would be a huge cut to their real income and they’d probably quit and find a better job. Enter high interest rates which makes borrowing expensive and encourages savings sapping demand from the economy. As consumer spending and investment falls, firms lay people off and retailers discount products. Our worker, facing a long spell of unemployment if they quit, can’t credibly bargain for a 6-8% cost of living adjustment (COLA) anymore. Slowly, painfully, inflation was ratcheted downwards by inflicting hardship on people.

Put these various elements together and you get a workable representation of how inflation works. The price level in the long run is based ultimately on the supply of money. The Keynesian demand story is the mechanism which makes this true. And when this mechanism doesn’t function for whatever reason, you won’t get the transmission of monetary expansion to rising prices. Finally, households and firms in the economy adapt to the level of inflation by changing their expectations which limits the real-world impact of monetary stimulus and helps to lock in the current level of inflation, either high or low. If inflation expectations become unmoored, drastic action is needed to reset them.

Currently we have two of the three ingredients for sustained inflation. The money supply has dramatically increased as the Bank of Canada began scooping up government bonds and other assets during the pandemic. The Keynesian transmission mechanism was supplied by the Federal government’s stimulus efforts. The last ingredient is inflation expectations. More on that below.

What is the Bank of Canada thinking?

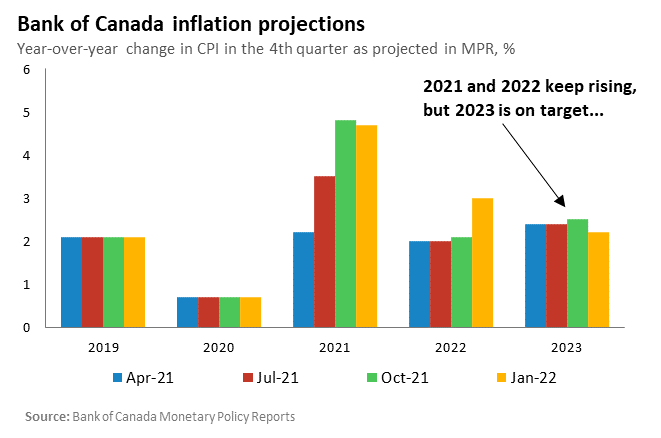

The view from the Bank of Canada is that the current wave of inflation is being caused by both supply chain disruptions and a wave of demand fueled by pandemic savings. Over the next year or two, supply chains will normalize, and as the economy reopens, spending will shift toward services which will reduce price pressures in the goods categories which have run up most. Eventually, people will have spent down the pools of savings they built during the pandemic and the wave of demand will relent. In other words, inflation will peak sometime this year and then fall of its own accord. As a bonus, 10-15% total inflation over this period will substantially erode the pandemic-related debt the government borrowed. While it could also help engineer a soft landing on housing, I think the evidence is actually the other way (more on that in a later post).

If the Bank’s view is correct, the error to be avoided is too many interest-rate hikes. The economy has mended, the central bank’s role now is to keep it growing on track. The Bank of Canada has a history of using low interest rates for a prolonged period to ease the economy through structural adjustments. For example, in 2015 when oil prices cratered, the Bank cut rates to help Alberta manage. By 2023 or 2024, interest rates will be a little higher than they are now, the pandemic will be in the rearview mirror, the labour market will be healthy, and inflation on target. Job done.

The risk is that after two or three years of high inflation, people’s inflation expectations will become unanchored. Instead of assuming inflation will be 2% over time, workers will ask for wage increases to preserve their buying power, or else quit and find a higher-paying job. The labour market is already very tight, meaning workers currently have an unusually strong bargaining position. In February 2022 and despite the Omicron wave, the overall unemployment rate was 5.5%. For prime-age workers (aged 25-54), it was only 4.4%. Both measures are now at their lowest level since the 1970s. Nearly half of firms report labour shortages and job vacancies are at an all-time high. Once workers begin to build in higher inflation when they negotiate wages, we are in a wage-price spiral that is tough to break.

Worse still, people can react to higher inflation by bringing forward their purchases. Since inflation was brought under control in 1990s the stock of cash sitting in Canadian chequing and savings accounts has increased dramatically and currently sits at about $1.3 trillion. After all, if inflation is low, the erosion of your wealth held in cash is usually imperceptible. People gripe about low rates on their savings accounts, but it doesn’t motivate them to put that money to work. That changes when inflation is high. People may start spending that money faster, anxious to buy products before prices rise further. If the so-called ‘velocity’ of money rises as people demand more of their wealth in cash to spend it, this multiplies the demand supported by each dollar in the economy and could cause inflation to spiral out of control.

Inflation Expectations

That’s why the Bank of Canada is so focused on inflation expectations. If they start to move in a meaningful way, or if people reveal their expectations in other ways — like wage demands — we may be heading down that more dangerous course. Unfortunately, signs are now beginning to appear that expectations are changing throughout the economy.

For consumers…

…for businesses…

…and for financial markets.7

If inflation expectations stay high and people and firms begin to act on them to make high inflation truly persistent, the Bank of Canada will have committed a grievous error. Interest rates will need to rise by a lot more to contain inflation, and given the state of the housing market, will almost certainly throw the economy into recession. The last time the Bank of Canada needed to raise interest rates to contain a rise in inflation was in the early 1990s. Interest rates rose by 6% and it caused a deep and long recession. That recession was made worse by high levels of government debt which forced spending cuts so debt payments could be made. We spent the 1990s and 2000s fighting to get our debt levels down, but now the public sector is right back to where we were.

Policymakers need to act fast

A recent report by Scotiabank included this arresting line: “The Bank of Canada’s credibility is very much on the line both in terms of the seriousness of addressing inflation and the stability issues associated with having overheated housing markets.” I think that’s right. The danger of underreacting to the current bout of inflation is now too high for policymakers to ignore. If inflation expectations continue to unravel, reestablishing low inflation will require a punishing increase in interest rates and a recession. That will devastate our overheated housing market for starters and pose unenviable trade-offs for governments. A soft landing from sustained high inflation is rare historically in economies like ours.

So much of economic trends are driven by sentiment and right now the sentiment is “I'm worried about inflation”. Historically, high inflation is accompanied by a loss of faith in government and a feeling of loss of control generally. At this point, a stronger signal is needed from policymakers that we are not on the verge of a spiral.

The Bank of Canada’s next meeting is on April 13th. At that meeting they should raise the policy rate by +0.75% — the equivalent of three hikes — and signal rates will continue to rise rapidly until inflation begins to come down. The neutral rate of interest is the rate at which monetary policy neither stimulates nor slows the economy. The best guess of that rate is about 2.25%. In other words, even after a big hike like that, monetary policy would still be accommodative. Given the unprecedented health of the labour market, there is no reason for the Bank to delay achieving the neutral rate. If they move fast enough, hopefully further action wont be needed.

There is a role for governments here too. Its budget season for the Feds and the Provinces and if last year is any guide, they will plot a very slow return to balanced budgets from their epic pandemic deficits. Indeed, the most recent projections show deficits extending to the end of the planning horizon — at least 4 years in most cases. The rapid rise in energy prices will help Alberta and Saskatchewan to close their gaps (and save Newfoundland and Labrador from disaster), but for the rest, further stimulus is now unwarranted and they should all credibly plan for as rapid a return to balanced budgets as practical. Now is not the time for new programs or tax cuts. Balance the books.

Plus imports minus exports for supply to the domestic market, but close enough.

The nominal value of a good is its value in terms of money. The real value is its value in terms of some other good, service, or bundle of goods.

As measured in the producer price index (PPI) which is also up around 10% year-over-year

As measured by capacity utilization

Taxes paid minus benefits received.

If money velocity — the number of times per year each dollar is spent — remains constant.

This chart from Scotiabank

Canada is in a real tough spot given just how big they allowed the housing bubble to grow. Unless Trudeau ups immigration to several million per year the rate increases needed to calm runaway inflation will pop the housing bubble